Co-authored with Mark Khalil

Deployment of renewables has been accelerating globally. In 2022, around 12% of electricity came from wind and solar, compared to less than 3% a decade ago. These resources offer access to low-cost clean energy – but only intermittently. Energy storage systems can capture excess renewable energy in times of abundance and discharge energy when sun and wind are scarce. Unfortunately, the development of storage assets has not kept pace with renewables, creating a massive storage gap. In this post, we will explore the storage gap and discuss three hypotheses on how it may get filled.

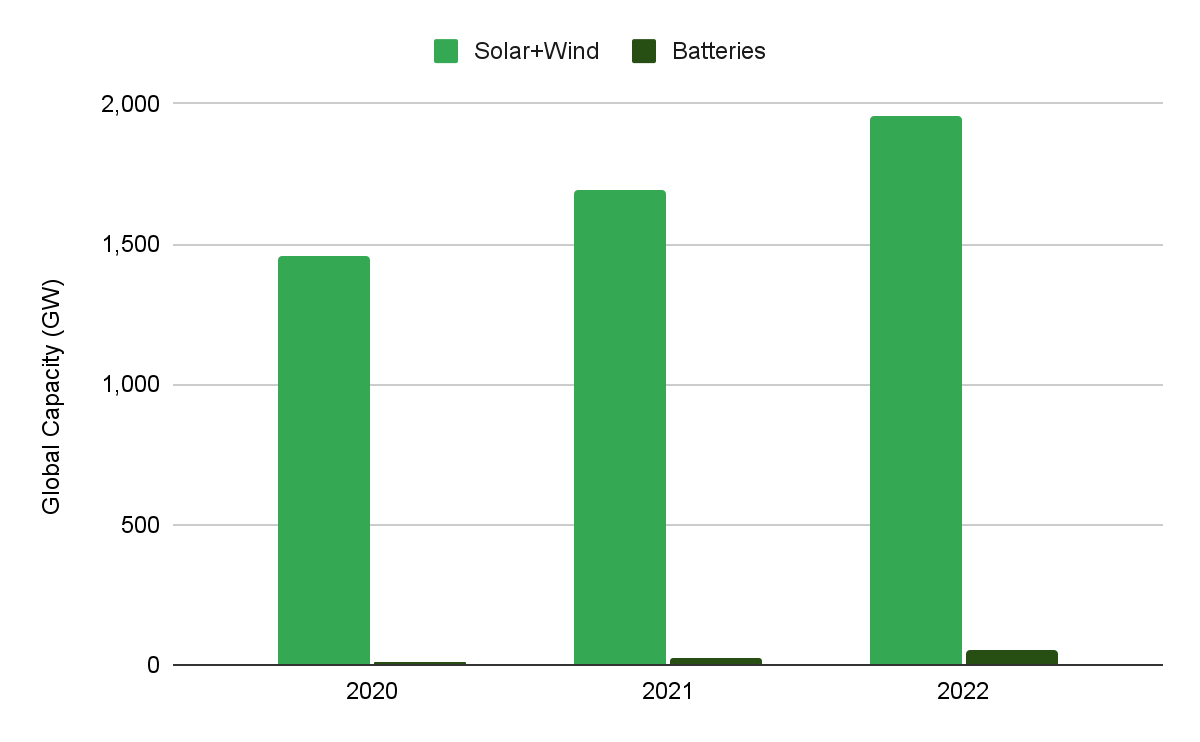

At the end of last year, the global supply of wind and solar stood at nearly 2 TW, while standalone batteries reached just over 50 GW (0.05 TW). Pumped-hydro offered another 175 GW (0.175 TW) of storage, though because of its required scale and siting restrictions, traditional pumped-hydro is limited in where and how quickly it can expand.

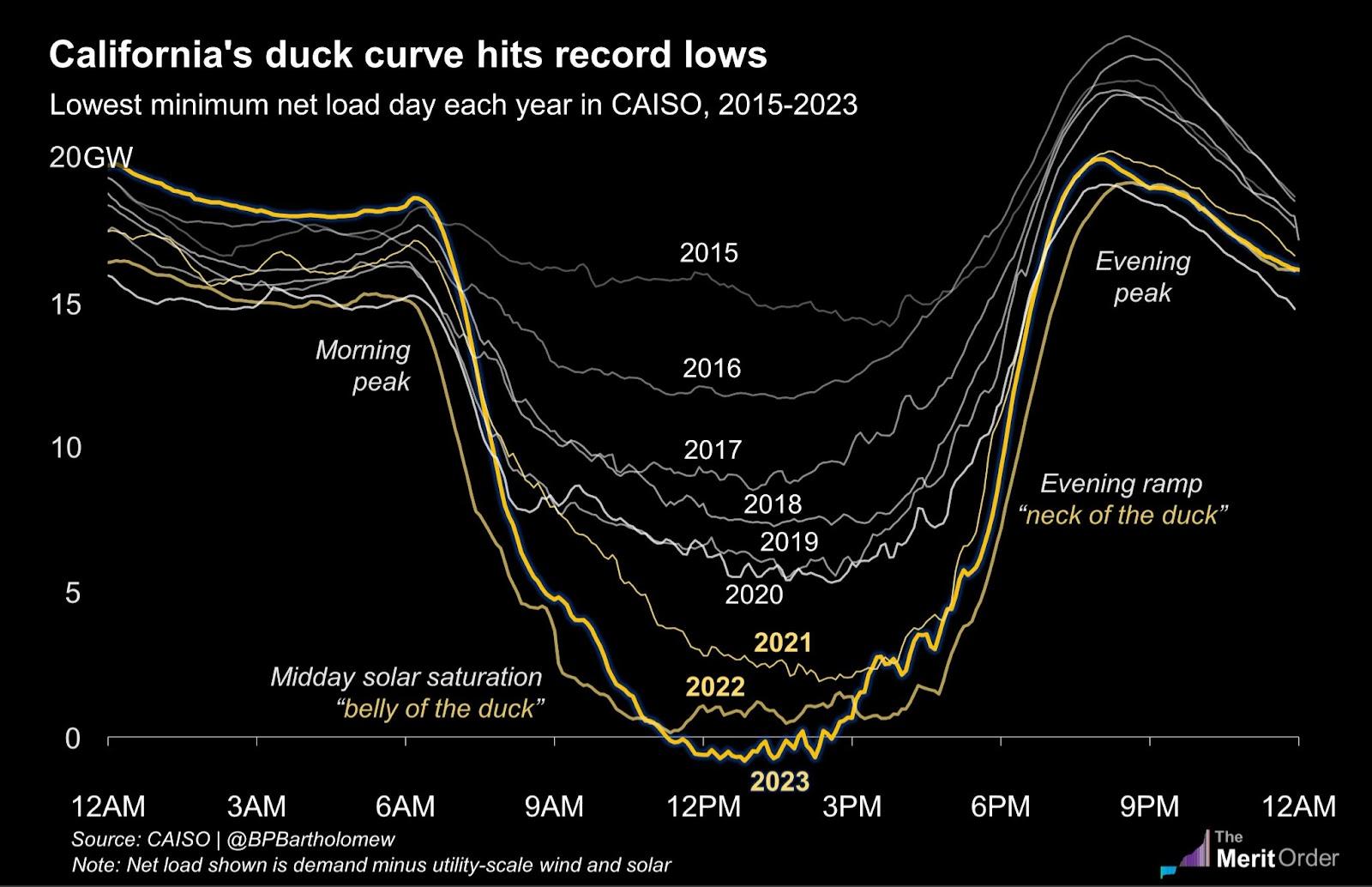

One way to understand the importance of closing the storage gap is to look at the disparity between power demand and supply of renewables throughout the day – the so-called “duck curve” (look at the yellow line to see the duck):

During daylight hours, there is often an excess of renewable energy, but when the sun sets, non-renewable sources have to quickly ramp up generation to meet demand. The sudden fluctuation poses a risk of grid instability if non-renewables cannot adjust in time. And the glut of power in the “belly of the duck” is so acute that there are increasingly frequent periods of negative electricity prices – even while prices remain high at other times. Energy storage offers a temporal bridge between times of abundance and scarcity of renewable energy, smoothing supply and demand and facilitating gains from trade across time.

The severity of the storage gap has created an opportunity to build transformational startups that will fundamentally change the shape of energy generation and distribution. As we look to invest in the space, we are exploring three hypotheses:

First, individual asset owners will aggregate their assets into networks instead of participating in storage markets themselves. Beyond storing energy for direct use, storage systems can create value by providing flexibility and ancillary services to the grid. However, most asset owners won’t have the expertise, resources, or risk tolerance to effectively take advantage of these capabilities on their own. Instead, they might opt to join a storage network where experts can virtually direct their assets and share the incremental value. Connecting storage assets could also unlock new services that no individual asset could offer, like access to different geographies depending on where the best opportunities are at a given time. Moreover, these virtualized networks can be agnostic with respect to the details of the underlying storage systems, enabling portfolios of batteries with different chemistries and non-stationary storage like EVs.

Second, storage has the potential to grow most quickly in the commercial and industrial (C&I) market as a result of the strong value proposition to C&I customers and fewer barriers to entry. Downtime in industrial processes can be extremely costly, making on-site energy storage an attractive backup for when the grid is down. And as C&I companies increasingly add behind-the-meter assets like solar and EV charging infrastructure, synergies between storage and those other applications make storage all the more valuable. Furthermore, given their scale, C&I customers are well positioned to invest in the bi-directional interconnects that enable storage assets to interact with the grid. C&I also has the advantage of generally being located where there is more space available to safely site batteries, which could pose a fire risk in other settings.

Finally, lithium-ion batteries will remain hard to compete with directly, suggesting the best storage startups will either leverage lithium-ion technology or counterposition with features that lithium-ion structurally cannot offer. The cost curve for lithium-ion looks similar to solar, dropping ~97% in the last 30 years and ~80% in just the last 10 years. As we continue to manufacture lithium-ion batteries at larger scales, our production processes will become even more efficient, further driving down costs. Because lithium-ion is already on such a steep learning curve, competing approaches cannot just be 10% cheaper or more efficient – they will have to be radically better along some other dimension. Such an approach might look like thermal storage for industrial plants with large heat needs or safer indoor-friendly batteries for urban areas with higher fire risks.

Addressing the storage gap represents an opportunity to supercharge the value of renewables and benefit both individual energy users and the grid itself. We are excited about innovative storage solutions that aggregate decentralized assets into networks, focus on C&I, and either leverage lithium-ion or offer unique features that lithium-ion cannot. If you’re working on building this future, we would love to hear from you.