Part 1: The 2.0-> 3.0 Transition

If mental health technology was like language-learning solutions, we have been in the language CD and tapes phase for the last decade or so.

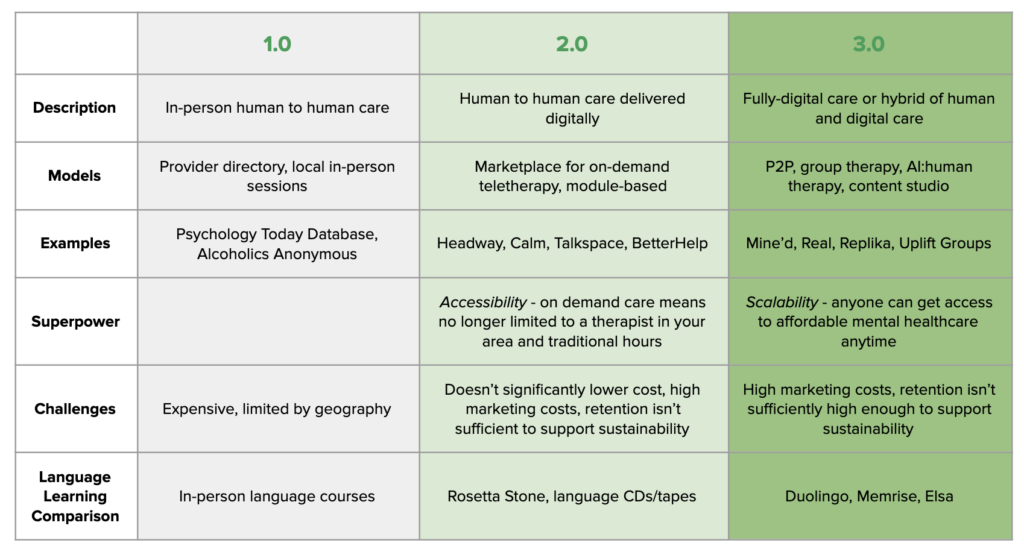

The shift from language textbooks to CDs was a 1.0->2.0 transition: it digitized the model of an in-person language class to scale learning across millions of new users on Rosetta Stone and other audio courses. The experience wasn’t personalized or dynamic, but it was cheaper and more flexible than signing up for an in-person course.

In a similar vein, mental health 2.0 companies re-built the traditional models of care — provider directories and marketplaces — in a digital way. Headspace, Meditopia and Calm expanded how and when one could practice meditation and mindfulness and built massive businesses. On-demand therapy platforms Talkspace and BetterHelp allowed patients to virtually find and visit therapists.

These were important, market-expanding companies: on-demand, virtual care meant users were no longer limited by local provider availability (60% of US counties don’t have a single psychiatrist). However, online therapy platforms still cost around $150-$300/month and are unaffordable for most US households. While the 2.0 wave of companies expanded access by lowering geographic boundaries to care, it didn’t fundamentally change the product itself in a way that inherently lowered cost. Meanwhile, the mental health crisis continues to grow: 1 in 5 US adults live with a mental illness, 61 percent of respondents to a January 2020 Cigna survey reported feeling lonely, and only 25% of affected children and adolescents receive treatment.

The more transformative shift in language-learning was 2.0->3.0: CDs to interactive mobile apps. Duolingo made language learning accessible to a huge audience around the world that could never afford a traditional language course by fundamentally changing the model of learning into one that is personalized, dynamic, and leverages network effects that improve the platform with every user interaction. Duolingo not only delivers a free and fun learning experience that feels more like a game than a classroom, but a social good: the translation of the web.

What does this mean for mental health 3.0 solutions? They will be interactive, adaptive, and buttery — more like Duolingo or Peloton than a MOOC or Rosetta Stone. In keeping with our thesis 3.0, we believe that the way to achieve unmatched scale and category creation is to leverage network effects.

3.0 companies fundamentally alter the traditional 1:1 therapist-patient model of care. The superpower of 3.0 is scalability by a leap, not a step, that drives down cost to broaden access while improving patient outcomes. These new models could take many forms: “user as producer”, AI, P2P, gaming, and group care are some that we are excited about. The most effective and interesting strategy may be a combined approach of 1:1 human interaction with scalable, community-driven P2P products and/or AI. One example might be a background AI layer that is able to digest 1:1 therapist-patient conversations and suggest peer groups as a follow-up.

There are also real challenges in the mental health category. Mental health is not a one-size-fits-all market, and product-driven strategies likely work better for some types of care than others. One roadblock to replacing mental health treatment with entirely self-service, AI-based care is that efficacy may not be a technological limitation, but a human one, particularly around acute issues.

Insurance coverage is one of the largest barriers to broadening access to care and figuring out how to get new products and services covered by payers is critical. 2.0 companies that bundled therapists into aggregated networks improved insurance rates and coverage, but as of 2019, behavioral health visits were still over five times more likely to be out-of-network than primary care. The shift towards digital treatment coverage is slowly underway; in March, Medicare temporarily changed its policies to cover most telehealth and many private insurance companies followed suit. The FDAs 2017 Digital Health Innovation Action Plan includes a regulatory model for digital health companies including manufacturers of digital therapeutics. Payors are increasingly open to covering digital solutions for pervasive and expensive illnesses, such as addiction, that often go hand in hand with other disorders.

There are opportunities across the spectrum from general wellbeing to severe illness to improve efficiency and efficacy. The former category may be more amenable to pure-play technological product improvements, whereas the latter may always require some interaction with clinicians to address acute patient needs but can leverage existing resources in a more efficient way while also helping patients learn to treat themselves and each other with less reliance on expensive and limited inpatient treatment.

In my next post, I will share four themes around what a 3.0 mental healthcare company might look like in practice.